The potential impact of high oil prices on economies

Prolonged high oil prices test global resilience, raising risks for growth, inflation, and monetary policy.

Prolonged high oil prices test global resilience, raising risks for growth, inflation, and monetary policy.

The ceiling for oil prices, and how long they’re high, is likely to be a matter of how long the conflict in Iran lasts. Prolonged hostilities would amplify economic effects and could further test investor resolve.

Vanguard analyses suggest that although the U.S. and global economies remain resilient, the scale and persistence of energy disruptions raise noteworthy risks for growth, inflation, and central bank decision-making.

An analysis by Fei Xu, portfolio manager of Vanguard Commodity Strategy Fund, highlights how quickly and significantly the oil shock has taken hold.

Notes: The front contract vs. 6-month-out contract premium/discount is a market-based measure of risk premia.

Sources: Vanguard calculations, based on Bloomberg data, as of March 9, 2026.

As the chart shows, the surge in oil prices and market based geopolitical risk premia have moved rapidly toward levels seen during the First Gulf War in 1990 and the Russia–Ukraine conflict in 2022. At those times, prices and risk premia rose sharply, remained elevated for several months, and gradually subsided only as supply conditions stabilized.

Transportation, insurance, and storage constraints are limiting export capacity throughout the Middle East energy complex, beyond oil production. If these constraints persist similar to situations in the past, macroeconomic consequences could become increasingly challenging. “If crude oil and natural gas disruptions, and the associated uncertainty, persist similar to 1990 or 2022, the macroeconomic spillovers would become increasingly stagflationary,” Xu says. “Sustained energy price shocks could push inflation higher, tighten financial conditions, and complicate policy tradeoffs.”

The costs of higher for longer oil prices would be felt most acutely in the euro area and Japan. A separate analysis shows that oil at $125 per barrel and natural gas at €150 per megawatt hour sustained for the rest of the year could trim a percentage point off euro area real GDP and drag the economy into recession.

“Sharply higher energy prices risk a stagflationary shock to the European economy,” says Shaan Raithatha, Vanguard senior economist. “Given this development, the European Central Bank may be forced to reassess its policy stance. Our bias is no longer to the downside.”

Elevated oil prices stemming from the Iran related conflict are likely to provide a modest tailwind for Canada, given its status as a net energy exporter. While higher energy costs may push headline inflation higher and weigh on household discretionary spending, the overall terms of trade effect should remain supportive for the Canadian economy.

Against this backdrop, the Bank of Canada (BoC) is expected to emphasize that financial markets are repricing risk in response to heightened geopolitical uncertainty, particularly in the Middle East. Policymakers are also likely to emphasize that there are no signs of financial system dysfunction, while noting that both the duration and geographic scope of the conflict remain highly uncertain. Importantly, the BoC is expected to reiterate that monetary policy cannot resolve geopolitical conflicts or offset supply side shocks. The BoC could be forced to tighten policy if inflation reaccelerates or if geopolitical developments, including the conflict in the Middle East, begin to lift inflation expectations. With yields having moved higher in Canada, some tightening related to the Middle East crisis has already occurred, even as Canadian labour markets continue to soften.

The analysis, however, highlights underlying strength in the U.S. economy. To induce a U.S. recession, oil prices would need to remain at $150 per barrel the rest of the year, and there would need to be a significant tightening of financial conditions, such as weaker asset prices and higher interest rates.

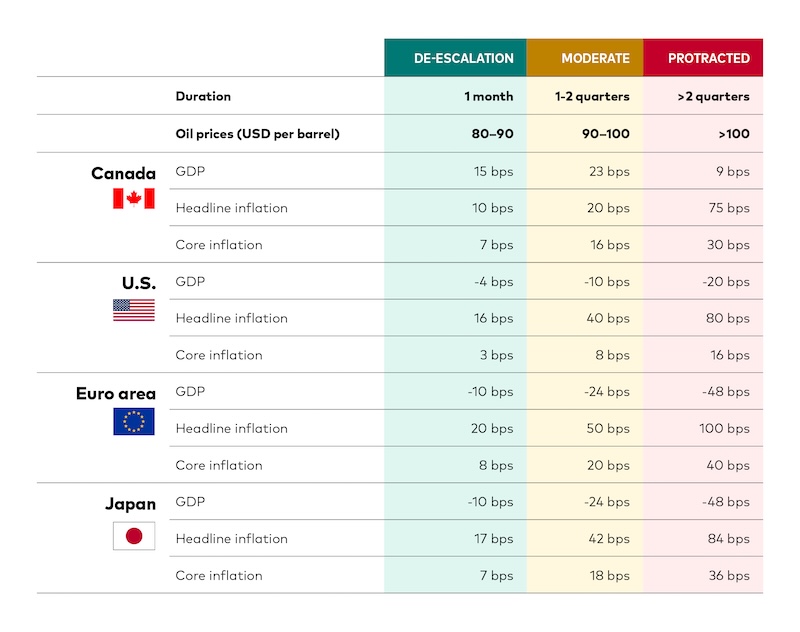

The table that follows shows anticipated economic effects of higher oil prices. Our assessment relies on history as a guide and considers variables such as offsetting impacts of fiscal and monetary policy. The effect on euro area inflation would be even greater if natural gas prices were also sustained at high levels.

Notes: Bps stands for basis points. A basis point is one-hundredth of a percentage point.

Sources: Vanguard calculations, based on Oxford Economics and Federal Reserve data, as of March 9, 2026.

The U.S. economy is comparatively well-positioned to absorb an energy shock, especially one that is shortlived. With household balance sheets, labor markets, and corporate fundamentals relatively strong, a deescalation of the conflict and a subsequent easing in oil prices could allow markets and economic activity to rebound. In that scenario, tighter financial conditions and weaker sentiment would likely unwind, limiting the risk of lasting damage and enabling a quicker snapback in growth and financial markets.

For now, continued conflict in the Middle East and high oil prices will likely tie central banks’ hands. Energy driven supply shocks are not something that monetary policy is designed to address, according to Josh Hirt, Vanguard senior U.S. economist. “Both sides of the Federal Reserve’s dual mandate fall under pressure,” Hirt said. “As long as it lasts, we would expect the Fed to have a bias toward inaction, although already elevated inflation will keep policymakers vigilant to potential changes in inflation expectations.”

Elevated oil prices would likely push out the timeline for rate cuts, Hirt said. Vanguard foresees just one Fed rate cut in 2026, a view that financial markets have adopted amid the conflict.

For the duration, Hirt said, investors will need to be prepared for what may lay ahead.

“Geopolitical uncertainty can pressure both stock and bond prices at the same time, even when the underlying economy is resilient,” he said. “Maintaining perspective and staying committed to a longterm strategy is a way for investors to navigate volatility and participate in any eventual rebound.”

Notes:

Publication date: March 2026

The information contained in this material may be subject to change without notice and may not represent the views and/or opinions of Vanguard Investments Canada Inc.

Certain statements contained in this material may be considered "forward-looking information" which may be material, involve risks, uncertainties or other assumptions and there is no guarantee that actual results will not differ significantly from those expressed in or implied by these statements. Factors include, but are not limited to, general global financial market conditions, interest and foreign exchange rates, economic and political factors, competition, legal or regulatory changes and catastrophic events. Any predictions, projections, estimates or forecasts should be construed as general investment or market information and no representation is being made that any investor will, or is likely to, achieve returns similar to those mentioned herein.

While the information contained in this material has been compiled from proprietary and non-proprietary sources believed to be reliable, no representation or warranty, express or implied, is made by The Vanguard Group, Inc., its subsidiaries or affiliates, or any other person (collectively, "The Vanguard Group") as to its accuracy, completeness, timeliness or reliability. The Vanguard Group takes no responsibility for any errors and omissions contained herein and accepts no liability whatsoever for any loss arising from any use of, or reliance on, this material.

This material is not a recommendation, offer or solicitation to buy or sell any security, including any security of any investment fund or any other financial instrument. The information contained in this material is not investment advice and is not tailored to the needs or circumstances of any investor, nor does the information constitute business, financial, tax, legal, regulatory, accounting or any other advice.

The information contained in this material may not be specific to the context of the Canadian capital markets and may contain data and analysis specific to non-Canadian markets and products.

The information contained in this material is for informational purposes only and should not be used as the basis of any investment recommendation. Investors should consult a financial, tax and/or other professional advisor for information applicable to their specific situation.

In this material, references to "Vanguard" are provided for convenience only and may refer to, where applicable, only The Vanguard Group, Inc., and/or may include its subsidiaries or affiliates, including Vanguard Investments Canada Inc.